The Effects of Technical Indicators on Exchange Rates: Empirical Insights from Quantile Regression Models

DOI:

https://doi.org/10.22452/mjs.vol44no3.7Keywords:

Exchange rate, Generalized lambda distribution (GLD), GLD regression, Quantile regression, Technical indicatorsAbstract

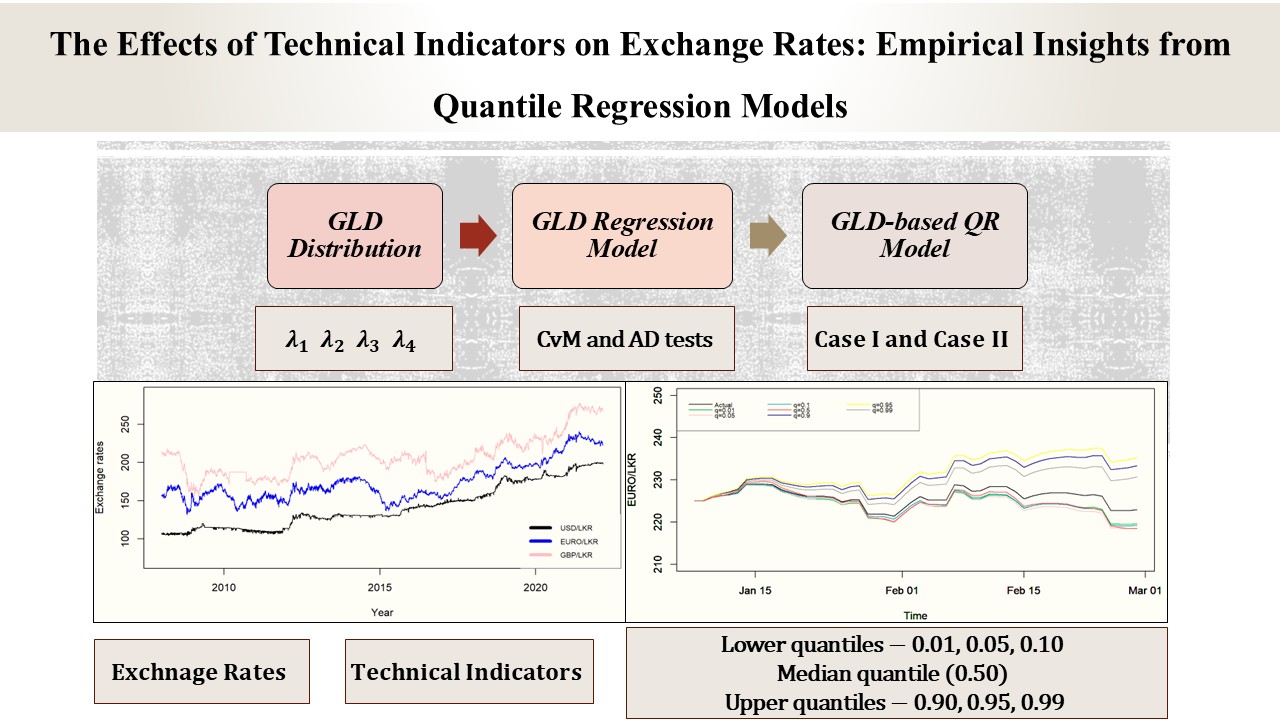

The modelling and forecasting of foreign exchange rates have proven challenging due to the prevailing extreme volatility and uncertain nature. Therefore, the primary objective of this investigation is to analyze and model the dynamics of exchange rates of the EURO, GBP, and USD against LKR using technical indicators of the previous day's low, high, and opening price, along with lagged and moving average (MA) values of closing prices. The generalized lambda distribution (GLD) regression models were employed in this study due to the non-normal behaviour exhibited by the error term. The GLD, being a versatile probability distribution, can encompass diverse distributional forms. Regarding the fitted GLD regression models, quantile regression (QR) models were utilised under two distinct conditions on closing price values of exchange rates: Case-I, coefficients were permitted to vary while maintaining a fixed intercept; Case-II, all coefficients were allowed to vary. The empirical study uses the daily data collected from the Yahoo Finance website from January 1, 2008, to February 28, 2022. Our findings show that the influence of technical indicators on exchange rate returns varies significantly across different quantiles. The models that demonstrated superior performance fall under Case-I, and based on the lower quantile of 0.1, for EURO/LKR with a mean absolute error (MAE) of 1.3246 and mean absolute percentage error (MAPE) of 0.0058, and for GBP/LKR with the minimum errors of MAE of 1.2253 and MAPE of 0.0045. For USD/LKR, the QR model fitted with the 0.5 quantile demonstrated the lowest errors with MAE of 1.1369 and MAPE of 0.0057. These findings hold significance as forecasts of exchange rates play an important role in financial decision-making processes.

References

Basnayake, B. R. P. M., & Chandrasekara, N. V. (2022). Forecasting exchange rates in Sri Lanka: a comparison of the double seasonal autoregressive integrated moving average models (DSARIMA) and SARIMA models. Journal of Science of the University of Kelaniya, 15(2), 192–209. https://doi.org/10.4038/josuk.v15i2.8067

Freimer, M., Kollia, G., Mudholkar, G. S., & Lin, C. T. (1988). A study of the generalized tukey lambda family. Communications in Statistics - Theory and Methods, 17(10), 3547–3567. https://doi.org/10.1080/03610928808829820

Huang, A. Y. H., Peng, S. P., Li, F., & Ke, C. J. (2011). Volatility forecasting of exchange rate by quantile regression. International Review of Economics and Finance, 20(4), 591–606. https://doi.org/10.1016/j.iref.2011.01.005

Kleopatra, N. (2008). The behaviour of the real exchange rate: Evidence from regression quantiles. Journal of Banking and Finance, 32(5), 664–679. http://hdl.handle.net/10419/153101

Lewis, C. D. (1982). Industrial and business forecasting methods: A practical guide to exponential smoothing and curve fitting. Butterworth Scientific.

Rodríguez del Águila, M. M., & Benítez-Parejo, N. (2011). Simple linear and multivariate regression models. Allergologia et Immunopathologia, 39(3), 159–173. https://doi.org/10.1016/j.aller.2011.02.001

Su. (2015). Flexible parametric quantile regression model. Statistics and Computing, 25(3), 635–650. https://doi.org/10.1007/s11222-014-9457-1

Su. (2016). Fitting Flexible Parametric Regression Models with GLDreg in R. Journal of Modern Applied Statistical Methods, 15(2), 768–787. https://doi.org/10.22237/jmasm/1478004240

Su, X., Zhu, H., You, W., & Ren, Y. (2016). Heterogeneous effects of oil shocks on exchange rates: evidence from a quantile regression approach. SpringerPlus, 5(1). https://doi.org/10.1186/s40064-016-2879-9

Tsai, I. C. (2012). The relationship between stock price index and exchange rate in Asian markets: A quantile regression approach. Journal of International Financial Markets, Institutions and Money, 22(3), 609–621. https://doi.org/10.1016/j.intfin.2012.04.005

Zhang, D., Wang, X., Gao, L., & Gong, Y. (2021). Predict and Analyze Exchange Rate Fluctuations Accordingly Based on Quantile Regression Model and K-Nearest Neighbor. Journal of Physics: Conference Series, 1813(1). https://doi.org/10.1088/1742-6596/1813/1/012016

Downloads

Published

Issue

Section

License

Copyright (c) 2025 Malaysian Journal of Science

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

Transfer of Copyrights

- In the event of publication of the manuscript entitled [INSERT MANUSCRIPT TITLE AND REF NO.] in the Malaysian Journal of Science, I hereby transfer copyrights of the manuscript title, abstract and contents to the Malaysian Journal of Science and the Faculty of Science, University of Malaya (as the publisher) for the full legal term of copyright and any renewals thereof throughout the world in any format, and any media for communication.

Conditions of Publication

- I hereby state that this manuscript to be published is an original work, unpublished in any form prior and I have obtained the necessary permission for the reproduction (or am the owner) of any images, illustrations, tables, charts, figures, maps, photographs and other visual materials of whom the copyrights is owned by a third party.

- This manuscript contains no statements that are contradictory to the relevant local and international laws or that infringes on the rights of others.

- I agree to indemnify the Malaysian Journal of Science and the Faculty of Science, University of Malaya (as the publisher) in the event of any claims that arise in regards to the above conditions and assume full liability on the published manuscript.

Reviewer’s Responsibilities

- Reviewers must treat the manuscripts received for reviewing process as confidential. It must not be shown or discussed with others without the authorization from the editor of MJS.

- Reviewers assigned must not have conflicts of interest with respect to the original work, the authors of the article or the research funding.

- Reviewers should judge or evaluate the manuscripts objective as possible. The feedback from the reviewers should be express clearly with supporting arguments.

- If the assigned reviewer considers themselves not able to complete the review of the manuscript, they must communicate with the editor, so that the manuscript could be sent to another suitable reviewer.

Copyright: Rights of the Author(s)

- Effective 2007, it will become the policy of the Malaysian Journal of Science (published by the Faculty of Science, University of Malaya) to obtain copyrights of all manuscripts published. This is to facilitate:

- Protection against copyright infringement of the manuscript through copyright breaches or piracy.

- Timely handling of reproduction requests from authorized third parties that are addressed directly to the Faculty of Science, University of Malaya.

- As the author, you may publish the fore-mentioned manuscript, whole or any part thereof, provided acknowledgement regarding copyright notice and reference to first publication in the Malaysian Journal of Science and Faculty of Science, University of Malaya (as the publishers) are given. You may produce copies of your manuscript, whole or any part thereof, for teaching purposes or to be provided, on individual basis, to fellow researchers.

- You may include the fore-mentioned manuscript, whole or any part thereof, electronically on a secure network at your affiliated institution, provided acknowledgement regarding copyright notice and reference to first publication in the Malaysian Journal of Science and Faculty of Science, University of Malaya (as the publishers) are given.

- You may include the fore-mentioned manuscript, whole or any part thereof, on the World Wide Web, provided acknowledgement regarding copyright notice and reference to first publication in the Malaysian Journal of Science and Faculty of Science, University of Malaya (as the publishers) are given.

- In the event that your manuscript, whole or any part thereof, has been requested to be reproduced, for any purpose or in any form approved by the Malaysian Journal of Science and Faculty of Science, University of Malaya (as the publishers), you will be informed. It is requested that any changes to your contact details (especially e-mail addresses) are made known.

Copyright: Role and responsibility of the Author(s)

- In the event of the manuscript to be published in the Malaysian Journal of Science contains materials copyrighted to others prior, it is the responsibility of current author(s) to obtain written permission from the copyright owner or owners.

- This written permission should be submitted with the proof-copy of the manuscript to be published in the Malaysian Journal of Science

Licensing Policy

Malaysian Journal of Science is an open-access journal that follows the Creative Commons Attribution-Non-commercial 4.0 International License (CC BY-NC 4.0)

CC BY – NC 4.0: Under this licence, the reusers to distribute, remix, alter, and build upon the content in any media or format for non-commercial purposes only, as long as proper acknowledgement is given to the authors of the original work. Please take the time to read the whole licence agreement (https://creativecommons.org/licenses/by-nc/4.0/legalcode ).